$4+ Billion OTC Dry Eye Drops Market Analysis Report 2026: Pfizer, Johnson & Johnson, and Novartis Lead

Introduction

The over‑the‑counter (OTC) dry‑eye drops market is projected to exceed $4 billion by 2026, driven by an aging population, increased screen time, and rising awareness of ocular health. This report breaks down the market dynamics, key players, and growth opportunities, giving beginners and industry enthusiasts a clear picture of where the sector is headed.

Market Overview

Why dry‑eye drops are in demand

- Demographic shift: People aged 45+ are the largest consumers, with prevalence rates of 15–30% worldwide.

- Digital eye strain: Mobile devices and remote work have doubled screen exposure, boosting symptoms.

- Health‑care accessibility: OTC availability removes prescription barriers, encouraging self‑treatment.

Market size and forecast

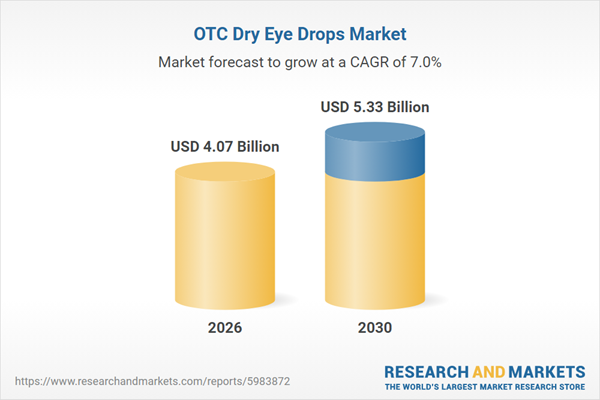

According to market intelligence, global OTC dry‑eye drops sales reached $2.9 billion in 2021 and are expected to grow at a CAGR of 9.5% to surpass $4.1 billion by the end of 2026.

Key Players and Their Strategies

Pfizer

Pfizer leverages its strong distribution network and continues to expand its Refresh line with preservative‑free formulations. Recent R&D investments focus on nanotechnology‑based lubricants that promise longer residence time on the ocular surface.

Johnson & Johnson Services

Johnson & Johnson dominates the retail shelf with the Visine and Retaine brands. The company’s strategy combines aggressive pricing, seasonal promotions, and a robust digital marketing campaign targeting millennials via social media influencers.

Novartis International

Novartis entered the OTC segment by acquiring the Systane portfolio. Their growth engine relies on cross‑promotion with prescription products and a focus on ophthalmology clinics that recommend OTC options to post‑procedure patients.

Competitive Landscape

While Pfizer, Johnson & Johnson, and Novartis command roughly 65% of market share, smaller niche brands differentiate themselves through organic ingredients, eco‑friendly packaging, or ultra‑light formulations for contact‑lens wearers.

Growth Drivers

- Regulatory support: Many countries have eased labeling requirements for OTC ocular lubricants, speeding time‑to‑market.

- Consumer education: Campaigns by eye‑health NGOs increase awareness of dry‑eye syndrome as a treatable condition.

- Innovation pipeline: Emerging technologies such as lipid‑based sprays and smart‑eye‑drop dispensers attract tech‑savvy users.

Challenges

- Potential over‑use leading to preservative‑related irritation.

- Price sensitivity in emerging markets where generic alternatives dominate.

- Stringent advertising rules for medical products in the EU and Canada.

Opportunities for New Entrants

Start‑ups can capture niche segments by focusing on:

- Natural, preservative‑free formulas (e.g., hyaluronic acid sourced from plant extracts).

- Subscription models delivering monthly supplies directly to consumers.

- Integration with tele‑ophthalmology platforms for personalized dosage recommendations.

Conclusion

The OTC dry‑eye drops market is poised for robust growth, with Pfizer, Johnson & Johnson, and Novartis setting the pace through product innovation, aggressive branding, and strategic acquisitions. Companies that prioritize consumer education, sustainable packaging, and digital distribution will be best positioned to capture a slice of the $4 billion opportunity by 2026.

Comments are closed, but trackbacks and pingbacks are open.